Rising inflation has made it difficult for hundreds of Florida homeowners to obtain affordable property insurance.

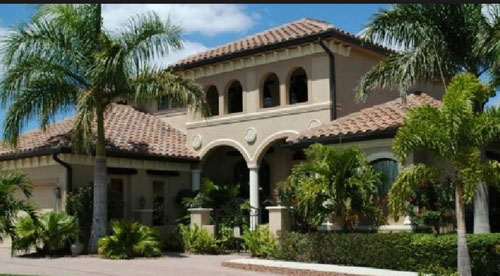

According to new data from Citizens Property Insurance Corp., Florida’s “insurer of last resort,” the company dropped 2,267 policies statewide during the 12-month period ending June 30 because the replacement value of their homes exceeded $700,000.

Except in Miami-Dade and Monroe counties, where Citizens can insure homes worth up to $1 million, this is the company’s eligibility limit in all counties.

If a new study by the state Office of Insurance Regulation finds that homeowners lack access to affordable coverage from private market insurers and have little choice but Citizens, the caps in Broward, Palm Beach, and other counties could be raised.

Citizens sent notices of non-renewal to 617 homes in Broward County over the last year with replacement values exceeding the $700,000 eligibility cap. 454 were dropped in Palm Beach County.

“The $700,000 coverage maximum is causing a lot of people to scramble to find coverage,” says Dulce Suarez-Resnick, vice president at Miami-based Acentria Insurance.

Unlike a home’s market value, which determines how much money you could get if you sold the house and the land it sits on, replacement values determine how much it would cost to replace a structure. While a hot real estate market can cause a home’s asking price to rise, replacement-value increases are caused by inflation, which raises the costs of building materials, energy, and labor.

Customers who continue to be eligible for Citizens coverage must pay higher premiums as a result of the increases.

However, owners who discover their homes are no longer eligible for Citizens are frequently forced to go without insurance, or, if they still have mortgages, to accept force-placed coverage from their mortgage servicer, or to purchase much more expensive coverage from excess and surplus lines carriers such as Lloyds of London.

Even excess and surplus lines insurers, which are not subject to state-mandated rate reviews and coverage requirements, are less likely to pick up business in South Florida, according to Suarez-Resnick.

“The excess and surplus lines markets in tricounty are almost at capacity, so they are being very selective,” she explained. Capacity refers to the amount of risk that a single company can accept in a given territory. If a company’s book of business is concentrated in a single territory, the company faces insolvency if a disaster generates more claims than the insurer can cover.

Many of the stranded homeowners had turned to Citizens in recent years after being dropped by a private-market insurer and unable to find another insurer willing to cover them at a reasonable price. Citizens has grown from 420,000 policies in 2019 to 938,437 as of July 1 as private market insurers have folded or stopped writing new policies in the state due to losses from high weather-related claims rates, contractor fraud, and opportunistic litigation.

Complaints from South Florida homeowners who were kicked out of Citizens prompted two state representatives — Robin Bartleman, a Democrat from Weston, and Chip LaMarca, a Republican from Lighthouse Point — to request a state study to determine whether the eligibility cap should be raised in counties other than Miami-Dade and Monroe.

The Office of Insurance Regulation confirmed in an email to Bartleman on Friday that it has agreed to investigate whether a lack of private market insurance competition warrants raising the eligibility cap. According to the office, the study will look at all 67 Florida counties.

This week, Bartleman expressed her delight at the news. “This is in the best interests of all Floridians who are having difficulty finding property insurance,” she wrote in an email. “Many homeowners are surprised to learn that their replacement cost exceeds $700,000 and had no idea Citizens Insurance could deny them coverage,” she explained.

The office has the authority under state law to raise the eligibility cap in counties where it determines there is a “reasonable degree of competition.”

Following a 2014 study, the office decided to exempt Miami-Dade and Monroe counties from a 2013 state law that reduced the eligibility cap from $1 million to $700,000 across the state. At the time, lawmakers were looking for ways to reduce Citizens’ 1.5 million policy count, and they thought homeowners with homes worth more than $700,000 were well off enough not to need Citizens’ safety net.

However, inflation has pushed the replacement value of homes that were in the $500,000 to $600,000 range a few years ago above the $700,000 cap, and more are on the way, according to Bartleman. She claims it is unjust to cover Miami-Dade policyholders up to $1 million while excluding owners of comparable homes in Broward and elsewhere.

The Office of Insurance Regulation’s Samantha Bequer said the new study will be conducted similarly to the 2014 study by analyzing multiple data points, including information from insurance companies, agents, and the office’s QUASR database, which insurers are required to update quarterly.

Bequer did not specify a completion date for the study, only saying that the office will provide updates “as they become available.”

The Florida Association of Insurance Agents’ president and CEO, Kyle Ulrich, stated last week that the FAIA’s board of directors also supported a new study. Ulrich stated that the association’s members would assist by providing a list of private market companies that are still writing policies in their respective counties.

Ulrich stated on Tuesday that he expects the number of Citizens non-renewals to rise in the coming year as Citizens continues to calculate replacement value increases.

With Citizens expected to reach 1 million policies by the end of the year, some lawmakers are likely to oppose any proposal that would increase the company’s risk of loss. Numerous legislators, as well as the chairman of Citizens’ board of directors, have expressed concern about Citizens taking on too much exposure.

If Citizens is unable to pay all claims following a disaster, state law allows special assessments to be levied first on Citizens policyholders, then on all property, commercial, and health insurance policyholders in the state.