RMS, a global risk modeling and analytics firm, has estimated that the insured loss for Hurricane Florence will be between USD $2.8 billion and USD $5 billion. This estimate represents insured losses associated with wind, storm surge, and inland flood damage across North Carolina, South Carolina, and Virginia, including losses to the National Flood Insurance Program (NFIP).

The estimate includes property damage and business interruption caused by wind, coastal flooding, and inland flooding to residential, commercial, industrial, and automobile lines of business. It also factors in post-event loss amplification. The figures also include estimated losses to the NFIP, which RMS expects to reach between US$800 million and US$1.2 billion.

Similar to events like Hurricane Harvey and Hurricane Irma in 2017, RMS expects uninsured precipitation-induced flood losses from Florence to be material due to the prolonged, record-breaking rainfall.

70 percent of flood losses are expected to be uninsured for this event. Accounting for uninsured wind, storm surge, and rainfall-driven flood losses in the U.S., RMS expects the overall economic loss from Hurricane Florence to fall between USD $6.0 billion and USD $11.0 billion. Economic losses, in this case, are losses to all potentially insurable properties, independent of whether they have coverage or not. It does not include items like roads and utilities, and government-owned property, which is often self-insured (or not at all).

Post loss amplification is included in these figures as RMS expects that prolonged recovery efforts will create interruption and amplify losses in the coming weeks and months. Florence caused significant damage to infrastructure in North and South Carolina, cutting off access to damage areas and further delaying the return of residents and reopening of businesses. Furthermore, the breadth of Florence’s impact in the southeast U.S., particularly from inland flooding, may produce a large volume of claims for insurers to address, leading to potential claims inflation. It is also possible that Assignment of Benefits issues, combined with an aggressive legal environment, may contribute to a heighted loss amplification status within the state.

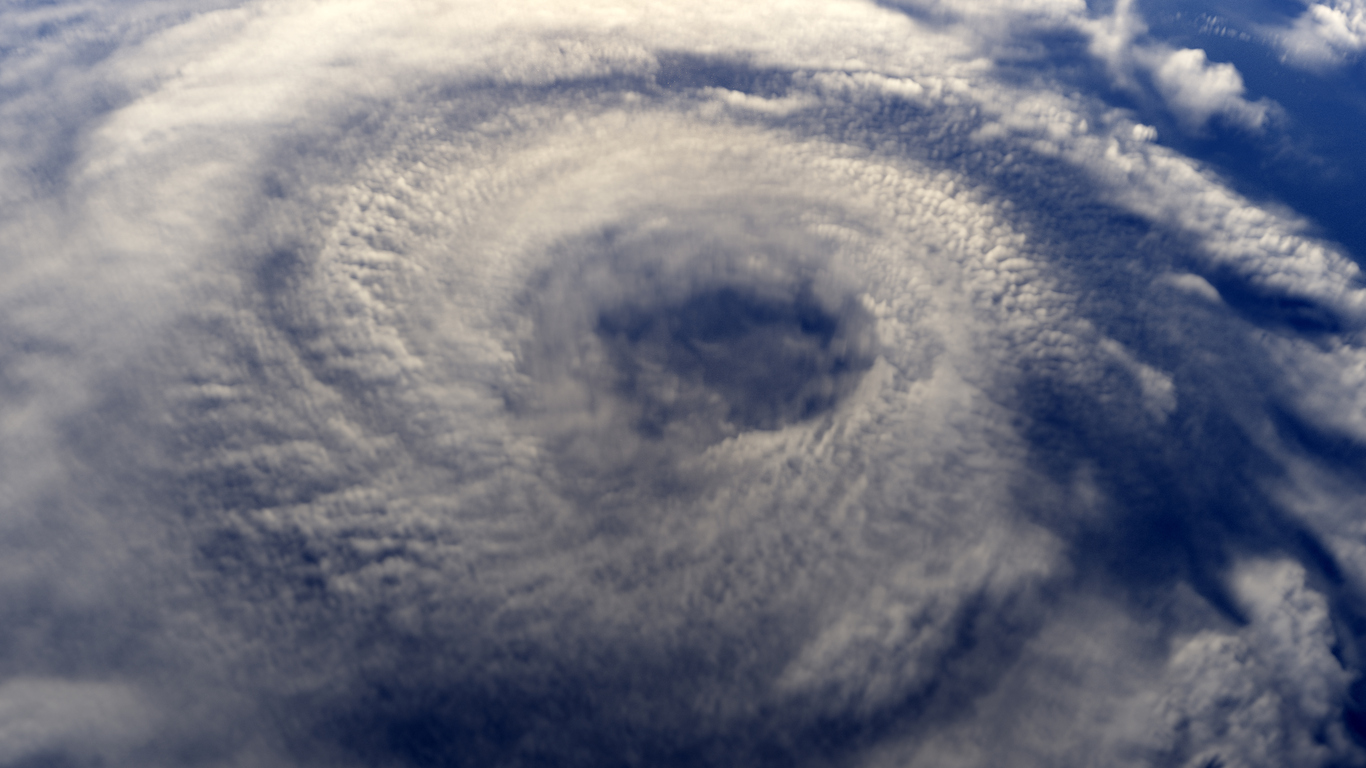

Hurricane Florence was the sixth named storm of the 2018 North Atlantic hurricane season. It was the first hurricane to make landfall in North Carolina since Hurricane Irene in 2011. Florence made landfall on Friday, September 14 near Wrightsville Beach, North Carolina as a Category 1 hurricane on the Saffir-Simpson Hurricane Wind Scale. Prior to reaching the U.S. mainland, Florence hit major hurricane status (Category 3 or greater), with sustained winds estimated by RMS HWind to have reached 127 miles per hour (204 km/hr). These wind speeds make it one of the most intense storms to navigate north of 30°N in recent history.

For this loss estimate, wind and storm surge impacts were simulated using version 18.0 RMS North Atlantic Hurricane Models and RMS ensemble footprints, which are hazard reconstructions of Florence’s wind field and storm surge

The upcoming RMS U.S. Inland Flood High Definition (HD) Model was also used to simulate the precipitation, run-off, and pluvial and fluvial flows through the southeast U.S. and Virginia.

Consistent with RMS event response efforts in recent years, RMS reconnaissance teams went onsite to survey the hazard and vulnerability impacts of Florence. Their detailed analyses further validated the RMS modeled extent and severity of the hurricane.

Mohsen Rahnama, Chief Risk Modeling Officer, RMS, said: “We were fortunate that Florence weakened considerably before making landfall as a Category 1 hurricane. While wind-driven damages will still be sizable, the story of this storm is the flood impacts. Florence’s slow moving nature brought historic rainfall and flooding to the Carolinas.”

“Florence is yet another large inland flood event that exposes the protection gap for flood insurance in the U.S. NFIP take-up rates are less than 1 percent for the vast majority of non-coastal counties in the North and South Carolinas. Thus, we expect much of the losses in interior portions of the region to be largely uninsured.”